Illinois’ largest medical malpractice insurer (ISMIE) is losing market share because of increased competition in Illinois – not because of lawsuits

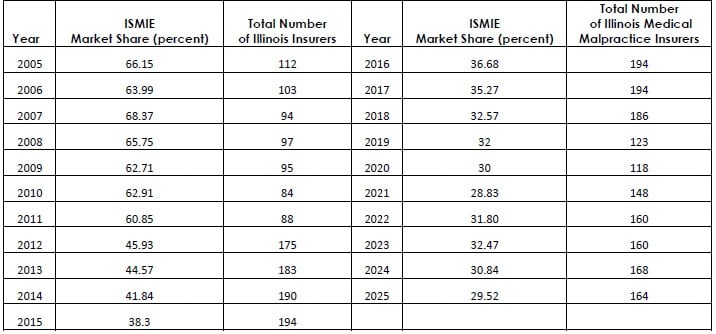

ISMIE is losing market share due to an increase in insurance companies doing business in Illinois. However, ISMIE is still by far the largest malpractice insurer in Illinois with 29.52% of the market, nearly six times as much as the next largest insurer.1 The substantial number of medical malpractice insurers doing business in Illinois indicates that malpractice insurers view Illinois as an attractive market and that typically means lower insurance premiums for doctors.

Recently, ISMIE has expanded into other states and other lines of business. They now write medical malpractice insurance policies in all 50 states and Washington D.C.2 This expansion has made ISMIE one of the nation's largest medical professional liability insurers.3

In Illinois, ISMIE’s annual reports reveal paid claims have fallen nearly 13 percent over the last decade. Costs for paid claims in Illinois have dropped just over 13 percent between 2015 and 2025.4

ISMIE’s direct written insurance premiums were just over $220 million in 2025. Overall assets approached $1.6 billion.5

ISMIE’s CEO’s annual compensation has exceeded $5 million in each of the last four years.6

Data compiled by the National Association of Insurance Commissioners (NAIC) makes clear that over the last decade, the medical malpractice insurance market has been extremely profitable nationally, that it has been even more profitable in Illinois than nationally; and that ISMIE has been more profitable than the Illinois average.7

1 Illinois Department of Insurance Market Share reports, various years. https://idoi.illinois.gov/reports.html

2 ISMIE Mutual Insurance Company 2025 annual report. https://www.ismie.com/ISMIE.com/media/ISMIEMediaLibrary/Documents/2025AnnualReport.pdf

3 Ibid.

4 ISMIE Mutual Insurance Company annual reports.

5 Ibid.

6 ISMIE Mutual Insurance Company Supplemental Compensation Exhibit.

7 NAIC Report on Profitability by Line by State 2023. April 2025.